By Tomas Karedin, Contributor | Somerset-Pulaski Advocate

Leading up to the primary election, the Somerset-Pulaski Advocate (SPA) received questions and concerns from the public about leadership in the Pulaski County Clerk’s Office, beginning in early 2025.

In response, SPA conducted a review of publicly available audit reports, open records requests, and additional public records that were shared. This report presents a document-based analysis of those materials to provide voters with context as they evaluate the office and its operations.

It is worth noting that we could not locate a 2025 Audit and assume, based on the dates on the previous audits, that it will be available later in the year. We encourage you to do an independent search for this and other documentation mentioned and listed in this article. If we have made an error in our analysis, we have provided the means for you to alert us and send supporting documentation so we can make appropriate edits. After all, as the sharp-witted poet, Alexander Pope, once said, "To err is human; to forgive, divine."

Here is the link to perform an audit search, not just for the County Clerk, but for all state public accounts:

Online Audit Search - Auditor of Public Accounts

Image source: Adobe Stock (licensed)

Audit Highlights

The 2023 and 2024 state audits of the Pulaski County Clerk’s Office both received an unmodified opinion on the regulatory basis of accounting, meaning the auditor found the financial statement fairly presented under Kentucky’s required regulatory accounting framework. However, both audits also note that the statements do not present fairly under U.S. generally accepted accounting principles because Kentucky fee-official audits use a special regulatory basis.¹²

For 2023, the Clerk’s Office reported $30,692,304 in total receipts and $29,839,599 in total disbursements, resulting in $728,320 in excess fees due to the county. The office paid $727,985 to Fiscal Court on March 12, 2024, leaving $335 due at completion of the audit.³

For 2024, the Clerk’s Office reported $30,194,972 in total receipts and $29,924,142 in total disbursements, resulting in $135,960 in excess fees due to the county. The office paid $134,638 to Fiscal Court on February 4, 2025, leaving $1,322 due at completion of the audit.⁴

A notable year-to-year change is the decline in excess fees due to the county, from $728,320 in 2023 to $135,960 in 2024—a decrease of $592,360.³⁴

The audits show higher operating and capital costs in 2024, including deputies’ salaries of $1,422,715, employer benefits of $417,334, lease-related costs, and capital outlay expenditures.⁴

The audits did not identify material weaknesses in internal control, but the auditor emphasized the review was limited and not designed to identify all possible deficiencies. Both audits also reported no instances of noncompliance or other matters required to be reported under Government Auditing Standards.⁵⁶

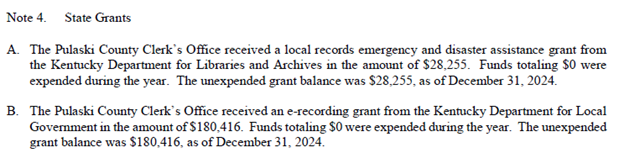

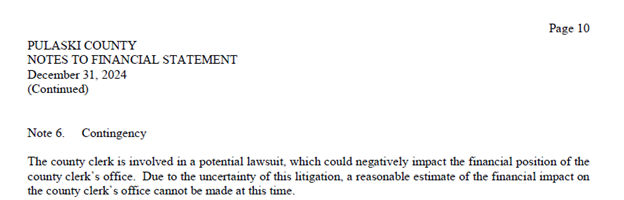

The 2024 audit includes two additional items voters may want to understand: the Clerk’s Office had unexpended grant balances of $28,255 (local records emergency/disaster assistance grant) and $180,416 (e-recording grant), and the audit disclosed a potential lawsuit that could negatively affect the office’s financial position, although the financial impact could not be reasonably estimated at the time.⁷

Bottom line: The audits do not show a state-reported material weakness or reportable noncompliance, but they do show a significant reduction in excess fees returned to the county between 2023 and 2024, along with ongoing operating costs, unspent grant funds, and a disclosed litigation contingency. These are legitimate public-finance questions for voters to examine.

Because excess fees represent funds returned to the county, significant year-to-year changes warrant clarification regarding whether the shift reflects normal operational investment, prior-year anomalies, or a structural change in how the office allocates its resources.

Staffing & Salary Trends

A February 2025 report indicated that nine employees were laid off from the Pulaski County Clerk’s Office. According to the Clerk, the layoffs were driven by declining revenues, delayed vehicle renewal notices attributed to a state vendor mailing issue, and reduced vehicle transfer activity. The Clerk stated that layoffs were based on seniority (most recent hires) and not performance, and that there was no guarantee of recall. Following the layoffs, the office reported a total of 26 employees.⁸

During the same period, the Clerk requested $225,000 from Fiscal Court to cover January payroll expenses, noting that the office begins the year with no available operating funds under the fee-office structure. This type of short-term funding request was described as not unusual within that framework.⁸

The Clerk’s Office salary records show that, despite the reported revenue concerns, hourly pay rates for multiple positions increased between 2022 and 2025. In 2022, deputy clerk positions generally ranged from approximately $12.00 to $26.10 per hour, with supervisory roles such as Chief Deputy or branch managers at the upper end of that range.⁹

By 2023, pay levels had increased across several classifications, with deputy clerks commonly ranging into the $14.00–$30.00 per hour range, and management roles (including Chief Deputy and branch-level leadership) reaching approximately $30.00 per hour.¹⁰

In 2024, the upward trend continued. Deputy clerk wages reached as high as $28.50 per hour, and the Chief Deputy

position increased to approximately $31.50 per hour, reflecting continued growth in compensation despite the broader revenue concerns cited publicly.¹¹

The 2025 reporting (as of June 9, 2025) shows continued elevated wage levels, with deputy clerks generally ranging up to $28.50 per hour and the Chief Deputy position remaining at approximately $31.50 per hour.¹²

From a staffing perspective, the June 2025 report lists approximately 25 positions, which is roughly consistent with the post-layoff staffing level reported in February 2025.⁸¹² There is no clear indication in the reporting that staffing levels returned to pre-layoff levels within that timeframe.

At the same time, the financial reporting included in the document reflects ongoing budget obligations and financial commitments, including multi-year financial commitments and operational expenditures tied to the Clerk’s Office budget structure.¹³

Bottom line: The available records show a reduction in staffing in early 2025, as indicated by fiscal court meetings and reports, alongside a multi-year upward trend in wages across positions, including leadership roles. While the layoffs were attributed to short-term revenue disruptions and broader economic conditions, the salary data reflects a parallel increase in compensation over time—an issue voters may reasonably weigh when evaluating budget management and staffing decisions.

Headcount goes ↓ Payroll goes ↑

| 2023 Audit | Amount | 2024 Audit | Amount | 2025 ORR* | Amount |

|---|---|---|---|---|---|

| Deputies' Salaries | $1,282,772¹ | Deputies' Salaries | $1,422,715² | Deputies' Gross Salaries *ESTIMATE (line 32) | 1,700,000¹³ |

| Employer Benefits | ~ $372,000 * | Employer Benefits | $417,334² | Employee Benefits *ESTIMATE (line 33 ) | $1,000,000¹³ |

| County Clerk's Gross Salary (line 30) | $142,000¹³ | ||||

| County Clerk's Expense Allowance (line 31) | $3,600¹³ |

*Open Records Request obtained by SPA: Form for Budget, Cumulative Quarter Report and Annual Settlement for Calendar Year 2025 - dated June 6, 2025

** Employer-paid benefits for 2023 are derived from the audit’s disbursement categories for payroll-related expenses, including retirement, FICA, insurance, and related costs.

Employee County & Hourly Range (2022-2025)¹³

| Year | Number of Employees Listed in Rate Schedule | Deputy Clerks Hourly Range | Chief Deputy Hourly Range | +/- |

|---|---|---|---|---|

| 2022 | 29 | $12.00 – $26.10 | $27.00 | -- |

| 2023 | 35 | $14.00 – $30.00 | $30.00 | 2022-2023: +11.1% |

| 2024 | 34 | $14.00 – $28.50 | $31.50 | 2023-2024: (+5.0%) |

| 2025 | 25 | $14.50 – $28.50 | $31.50 | 2024-2025: flat |

Editorial Analysis: Key Financial & Operational Questions for Voters

The state audits of the Pulaski County Clerk’s Office do not report material weaknesses or findings of noncompliance. At the same time, the audits, salary records, and recent reporting together present a more complex picture—one that raises legitimate questions about how the office is managing revenue variability, personnel decisions, and longer-term financial obligations.¹⁴

One of the clearest financial signals is the sharp decline in excess fees returned to the county. In 2023, the Clerk’s Office returned $728,320, while in 2024 that amount fell to $135,960—a decrease of more than $592,000 year over year.³⁴ The audits show the financial components of the change, but they do not explain the policy or management decisions behind it.⁴ This shift is significant because excess fees represent funds returned to the county and, ultimately, to the public.

Staffing and compensation trends add another layer to that picture. In early 2025, the office reduced its workforce by nine employees, citing revenue pressures and external factors affecting collections.⁸ At the same time, available salary records show a multi-year pattern of increasing hourly rates across positions, including leadership roles.⁹¹⁰¹¹¹² The records do not establish a causal relationship between these factors; however, they do show a smaller workforce operating during a period in which compensation levels increased—an alignment that may reasonably prompt questions about how staffing and compensation decisions are balanced over time. The records also do not provide context regarding cost-of-living adjustments, market conditions, or broader compensation trends that may have influenced these changes.

The structure of the office’s finances further shapes how these issues should be understood. Under Kentucky law, county fee officials are required to remit excess fees to the fiscal court annually rather than retain them for future operations.¹⁵ ¹⁶ In practice, this has required the office to request short-term financial support from Fiscal Court to cover early-year expenses, including payroll.⁸ This cash-flow dynamic is not unique to the Clerk’s Office; similar conditions can apply to other fee offices operating under the same statutory framework. However, the scale, timing, and management of these short-term funding needs remain appropriate areas for public consideration.

Earlier financial reporting provides additional context for these year-to-year changes. Records from 2022 reflect the Clerk’s Office operating within a same general multi-million-dollar fee-office revenue pattern, suggesting that the elevated excess fees reported in 2023 may not represent a long-term baseline but rather a higher point within a multi-year cycle.¹7

Quarterly reporting from late 2024, while not subject to the same audit process, also provides a snapshot of the office’s financial position immediately preceding the staffing changes and early-year funding request.¹8 Viewed together, these records suggest that both increased expenditures and normal variation over time may have contributed to the decline in excess fees, rather than a single-year anomaly.

Additional factors reflected in the records include more than $200,000 in unspent grant funds and ongoing multi-year commitments for technology and equipment.⁷ These items are not inherently problematic, but they contribute to the overall financial context in which budget decisions are made. The 2024 audit also notes a potential legal contingency, the financial impact of which could not be determined at the time of reporting.⁷ (See audit snapshots below)

2024 Audit, page 9

2024 Audit, page 10

In addition to financial considerations, SPA has received multiple communications from members of the public expressing concerns about hiring practices and internal management within the office. Under Kentucky law, public officials are subject to statutory ethics provisions governing conflicts of interest and certain employment relationships.¹9 These provisions are highly fact-specific and depend on circumstances such as the timing of employment, supervisory authority, and whether compensation and position changes were made through established administrative processes. The records reviewed for this publication do not independently establish a violation of those provisions. At the same time, questions about hiring practices, compensation adjustments, and internal oversight remain matters of legitimate public interest.

Clerk's Role in Elections

It is also important to note that the Clerk’s Office also carries statutory responsibilities for administering elections, as reflected in the review of the post-election reporting following the 2024 general election.²⁰ While that reporting is operational in nature and separate from financial audits, it highlights the breadth of duties managed by the office.

Upon reviewing the 2024 General Election After Election Report submitted to the State Board of Elections,²⁰ the report indicates that the Clerk’s Office processed 1,818 absentee mail-in ballot requests, of which nine were cancelled and nine replacement ballots were issued. The office also received 49 Federal Post Card Applications (FPCA), of which 40 were returned and processed on or before election day.

On election day (Nov 5, 2024), the Clerk’s Office processed 1,698 returned absentee mail-in ballots and reported 1,420 mail-in ballots in the official election-night results.²⁰ The report further notes that 58 ballots were rejected due to deficiencies, including issues such as missing signatures or improper envelope handling.²⁰

On December 2, 2024, the State Board of Elections contacted the Clerk’s Office regarding a discrepancy in ballot totals, initially estimated between 250 and 275 ballots.²⁰

In response, the Clerk’s Office obtained a court order to open the ballot-counting machines and verify the physical ballot count, which totaled 1,420 ballots.²⁰

A subsequent reconciliation, including a count of processed ballot records (‘slips’, as described in the report), identified 1,640 absentee ballots, and when combined with 40 FPCA ballots, resulted in a total of 1,680 ballots cast.²⁰

Image by Edmond Dantes | Pexels

This produced a difference of 260 ballots (1,680 – 1,420).²⁰

The report characterizes this as a discrepancy in ballot accounting between the initial election-night reporting and the totals identified through post-election reconciliation. It further notes that no races were decided by a margin of 260 votes.²⁰ The report does not conclude that ballots were lost or uncounted, but rather reflects a discrepancy identified and addressed through post-election reconciliation procedures.

The original document uses the term ‘missing ballots’; however, the records reviewed here reflect a discrepancy in ballot accounting rather than independently establishing that ballots were lost or uncounted.

SPA will request similar documentation for this election when it becomes available.

Conclusion

These records do not establish wrongdoing. They do, however, present a set of facts that warrant careful consideration: a substantial reduction in excess funds returned to the county, workforce reductions during a period in which compensation levels increased, and the use of short-term funding to meet early-year operating needs.

The use of short-term funding is not unique to the Clerk’s Office and can occur under Kentucky’s statutory framework for fee offices, which requires annual remittance of excess funds. As such, the relevant questions are not whether these practices occur, but how they are managed in terms of timing, scale, and planning.

In an elected office responsible for managing public funds, these are not minor issues. They are questions of financial management, planning, and transparency that voters may weigh as they make their decision.

With just over two weeks until the primary election, now is the time to ask questions, engage in conversation, and understand the issues. Take the time to consider the information and ask questions before you vote. Voting is both a privilege and a responsibility.

Image by Cottonbro Studio |Pexels

Footnotes

¹ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2023 (Frankfort, KY: Auditor of Public Accounts, July 26, 2024), 1.

² Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024 (Frankfort, KY: Auditor of Public Accounts, October 1, 2025), 1.

³ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2023, 6.

⁴ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024, 6.

⁵ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2023, 15–16.

⁶ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024, 13–14.

⁷ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024, 9–10.

⁸ Carla Slavey, “County Clerk’s Office Lays Off 9 Workers,” Commonwealth Journal (Somerset, KY), February 4, 2025, as republished by Yahoo News.

⁹ Pulaski County Clerk’s Office, Employees Rate Per Hour (As of December 31, 2022), in “Request, Salaries, and 2025 Financial Reporting” document, 3.

¹⁰ Pulaski County Clerk’s Office, Employees Rate Per Hour (As of December 31, 2023), in “Request, Salaries, and 2025 Financial Reporting” document, 4.

¹¹ Pulaski County Clerk’s Office, Employees Rate Per Hour (As of December 31, 2024), in “Request, Salaries, and 2025 Financial Reporting” document, 5.

¹² Pulaski County Clerk’s Office, Employees Rate Per Hour (As of June 9, 2025), in “Request, Salaries, and 2025 Financial Reporting” document, 6.

¹³ Pulaski County Clerk’s Office, Form for Budget, Cumulative Quarterly Report and Annual Settlement (2025), in “Request, Salaries, and 2025 Financial Reporting” document, 7–13.

¹⁴ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2023 (Frankfort, KY: Auditor of Public Accounts, July 26, 2024), 15–16; Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024 (Frankfort, KY: Auditor of Public Accounts, October 1, 2025), 13–14.

¹⁵ Kentucky Auditor of Public Accounts, Report of the Audit of the Pulaski County Clerk for the Year Ended December 31, 2024, 7.

¹⁶ Ky. Rev. Stat. Ann. § 64.152; § 64.820.

17 Pulaski County Clerk’s Office, 2022 Financial Reporting (Pulaski County, KY, 2022).

18 Pulaski County Clerk’s Office, 2024 Q4 Financial Reporting (Pulaski County, KY, 2024).

19 Ky. Rev. Stat. Ann. § KRS 65.003; see also applicable local ethics ordinances governing conflicts of interest and employment relationships.

²⁰ Pulaski County Clerk’s Office, 2024 General Election After Election Report to State Board of Elections (Pulaski County, KY, 2024).

This publication is based on publicly available records and audit documentation. While every effort has been made to ensure accuracy, errors or omissions may occur. Readers are encouraged to contact Tomas Karedin at info@somerset-pulaski-advocate.org with any corrections, clarifications, or additional documentation.

The Somerset-Pulaski Advocate (SPA) is an independent publication. SPA does not receive funding from, nor does it endorse or support, any political candidate or campaign. Content is intended for informational and public-interest purposes only and should not be construed as legal or financial advice. The Somerset-Pulaski Advocate is an independent publication. The views expressed in articles, commentary, and analysis are those of the authors and contributors and do not represent the views or positions of any government agency, employer, contractor, or affiliated organization.